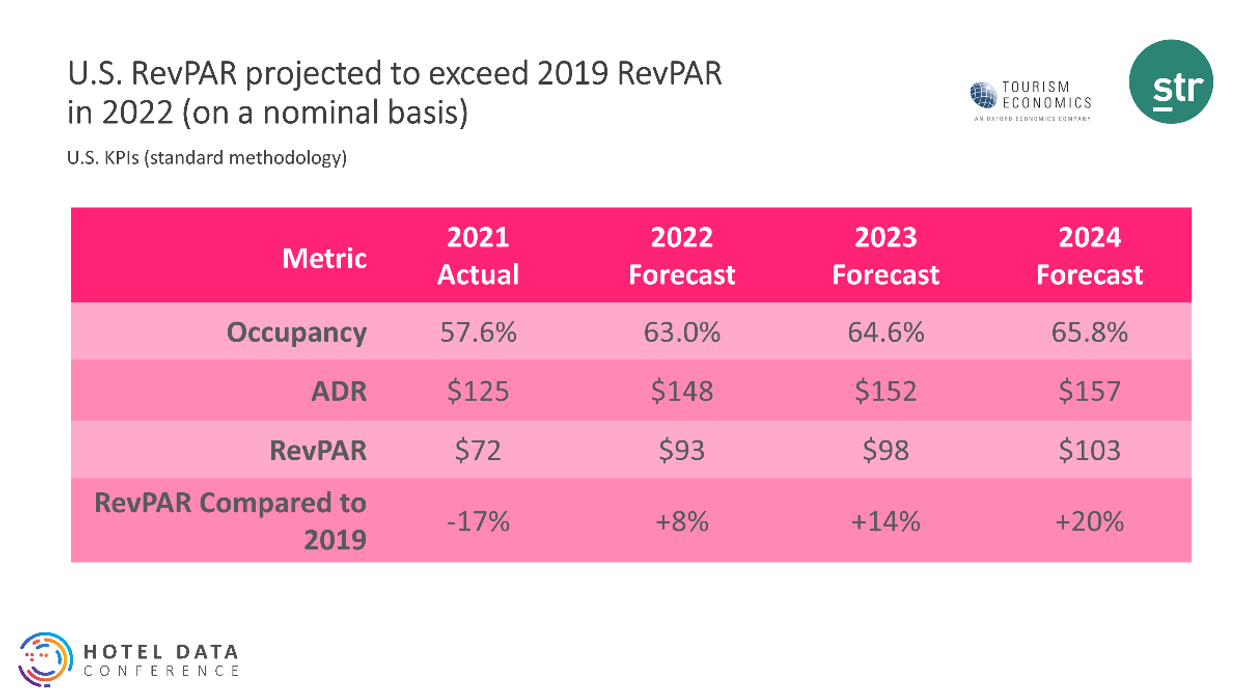

OCCUPANCY PROJECTIONS ARE dropping while ADR projections are rising in a new forecast for U.S. hotels by STR and Tourism Economics. RevPAR is still expected to recover fully on a nominal basis this year, according to the forecast released Thursday at STR’s 14th Annual Hotel Data Conference in Nashville.

However, RevPAR is still expected to take until 2025 to recover when adjusted for inflation, according to the forecast. For 2022, RevPAR is now expected to average $93 compared to the projection of $92 released in June, when projected nominal RevPAR recovery was set in 2023.

The occupancy projection for the year was lowered to 64.6 percent for the year and the ADR projection rose to $148. The updated forecast adds a little more than $2 to the ADR projection for both 2022 and 2023, and occupancy was lowered by less than a percentage point for each year.

“Leisure demand, as expected, hit significant levels this summer, and what we are hearing in earnings calls and from our industry colleagues would indicate that group business travel should be much more aligned with pre-pandemic patterns in the fall and winter,” said Amanda Hite, STR president. “Our downward adjustment to occupancy was pretty much focused on a slowdown in the economy segment, which is likely due to a mix of leisure travelers wanting higher levels of accommodation and budget travelers being priced out of the market. Inflation remains the key consideration in our ADR discussions, but hotels continue to display strong pricing power. There are reasons to be concerned about the economy, continued challenges around labor and business transient still lagging, but the hotel industry is on solid footing. U.S. profitability hit a 32-month high in June, and margins have remained strong although some reduction is likely with higher staffing levels, wages, and costs.”

STR and TE do not expect a recession, however, said Aran Ryan, TE’s director of lodging analytics.

“The baseline Oxford Economics outlook anticipates slow economic growth in 2023 but not a recession, as a combination of cooling aggregate demand and easing supply constraints will help slow inflation,” Ryan said. “In this context, with leisure demand supported by solid household finances and an ongoing recovery of group and business travel, lodging performance gains are expected to continue, though at a much slower pace than experienced this year.”

This year’s HDC is sold out, STR announced earlier this week.