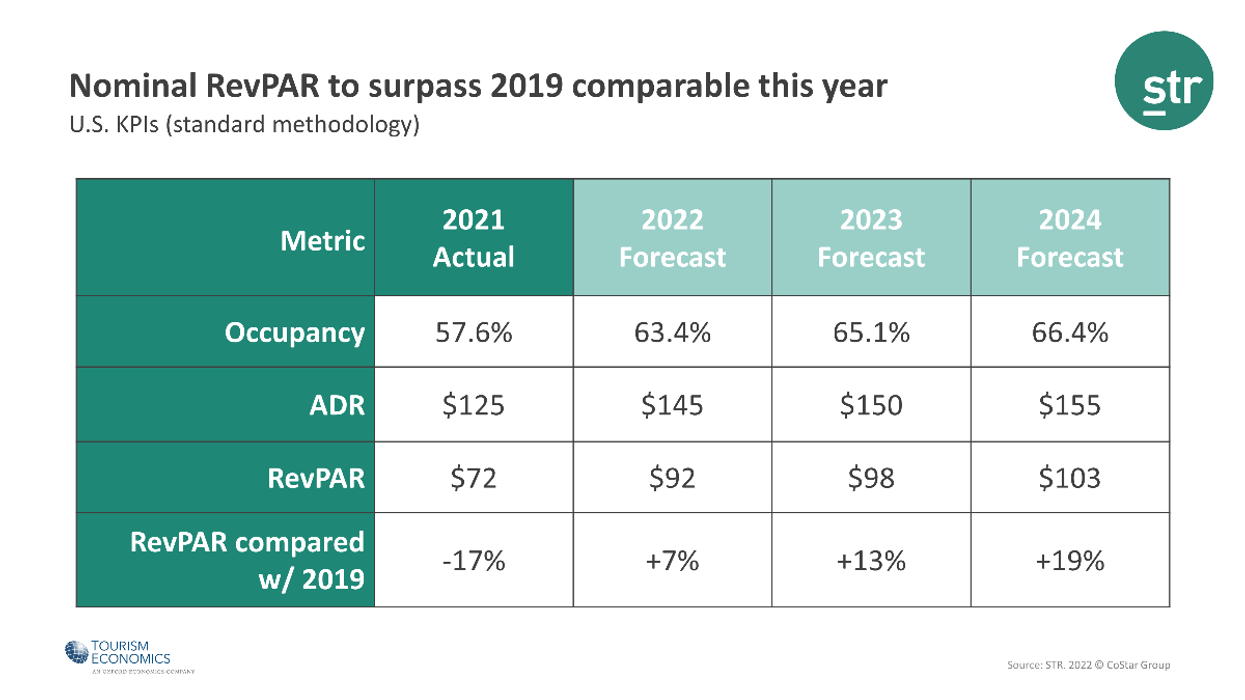

THE REVPAR OF U.S. hotels is expected to surpass 2019 levels this year, according to the upgraded forecast by STR and Tourism Economics. Still, full recovery may be a couple of years away.

ADR and RevPAR for U.S. hotels are forecasted at $14 and $6 higher in 2022 respectively, when compared to 2019, the report presented at the 44th annual NYU International Hospitality Industry Investment Conference stated. However, occupancy in this year is projected to come in under the pre-pandemic comparable.

Earlier, the forecast projected nominal RevPAR recovery in 2023.

According to the forecast, the major factor in the revised timeline was a plus $11 adjustment in 2022 ADR. But, when adjusted for inflation, full recovery of ADR and RevPAR are not projected until 2024.

The report added that central business districts and the top 25 markets are not expected to reach full RevPAR recovery until after 2024.

“Demand and occupancy have trended well in line with our recent forecasts, but pricing continues to exceed expectations due to the influence of inflation as well as the economic fundamentals supporting increased guest spending,” said Amanda Hite, STR president. “This latest forecast acknowledges the risk of a light recession with no anticipation of mass layoffs and household finances in a strong position to mitigate recession impacts. The traveling public is less affected by recession, and right now, we are forecasting demand to reach historic levels in 2023 as business travel recovery has ramped up and joined the incredible demand from the leisure sector. Concerns persist around the cost of labor and services, and hotels in some major markets are still well behind in the recovery timeline.”

“The outlook for hotel performance remains positive,” said Aran Ryan, director of lodging analytics at TE. “Even as the economy faces headwinds of higher interest rates, volatile financial markets, and inflation, lodging demand and room rates are being buoyed by strong household finances and the return of business travel.”

“With the Federal Reserve rapidly tightening monetary policy to tame inflation, there is a risk that financial conditions, which remain very accommodative, start to tighten in a disorderly manner,” said Adam Sacks, president, TE. “This would risk abruptly slowing the flow of credit and weigh on corporate and business confidence, which would further restrain economic growth. Should a U.S. recession occur, it is anticipated to be less severe than the Great Financial Crisis, due to lower current overhang of financial imbalances."