- JLL: Hotel debt unaffected by uncertainty, private credit concerns.

- Hotel transactions rose 14.4 percent in Q1 to $5.6B, driven by luxury deals.

- Institutional investors are increasing interest in hotel investment.

GEOPOLITICAL UNCERTAINTY AND private credit concerns have not affected hotel debt liquidity, according to JLL Hotels & Hospitality Group. Through March, RevPAR rose, with a split in performance: luxury hotels up 7.3 percent and economy hotels down 2.1 percent.

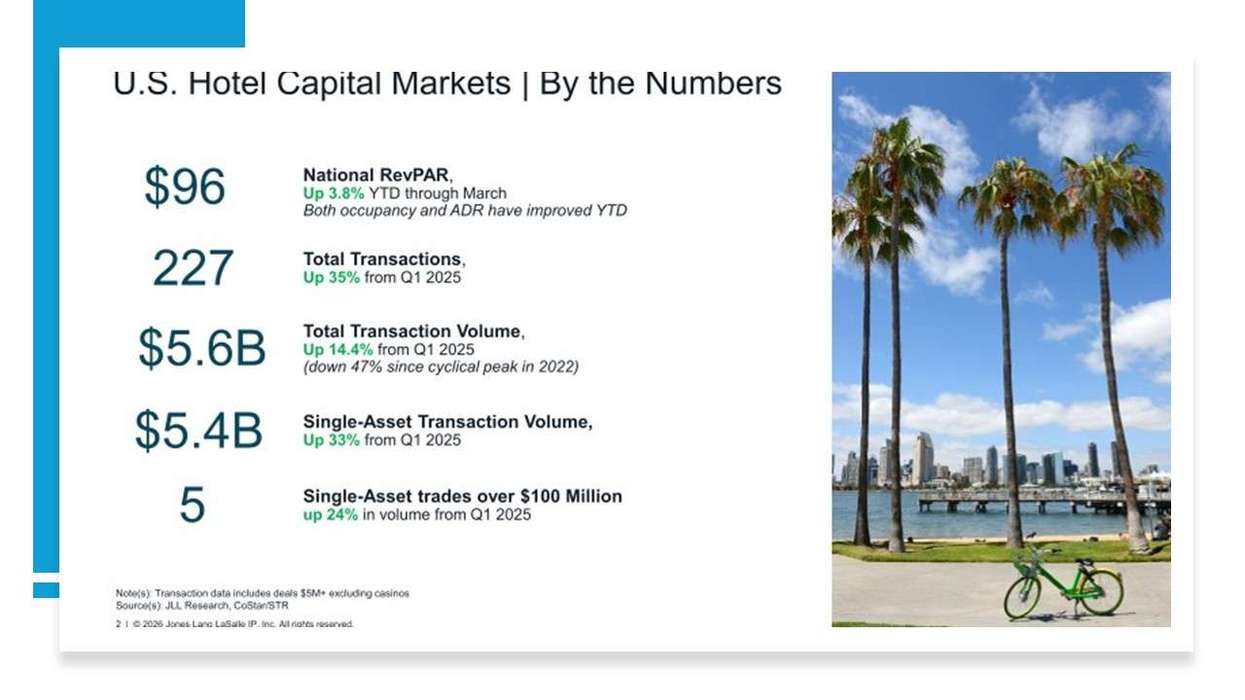

JLL’s “U.S. Hotel Investment Market Update” found U.S. RevPAR at $96, up 3.8 percent year to date through March, with occupancy and ADR also up year to date.

Hotel transactions rose 14.4 percent in the first quarter to $5.6B, driven by several luxury deals. JLL recorded 227 hotel transactions, up 35 percent year over year.

Analysts attributed private equity demand in hotels, which accounted for 34 percent of transaction volume, to stabilizing interest rates and market conditions.

Quarterly transaction volume was $5.6 billion, up 14.4 percent from quarter one 2025 and down 47 percent from the 2022 peak. Full-service and select-service assets continue to trade below replacement cost.

Single-asset transaction volume was $5.4 billion, up 33 percent year over year, including five sales above $100 million. The report also noted slower supply growth, which could underpin existing hotel performance.

Institutional investors—including private equity firms, REITs and high-net-worth individuals—are increasing interest in the hotel sector, JLL said. The interest is driven by yields compared with other commercial real estate classes and confidence in the sector.

Large-scale transactions are expected to lead the market and improved debt conditions are expected to support more high-value asset and portfolio sales.

In February, JLL found global hotel transaction volumes rose 22 percent from the 2023 trough in 2025, with the Americas up 27 percent. Hotels accounted for about 8 percent of global commercial real estate investment, above the long-term average, supported by slower supply growth in major markets.