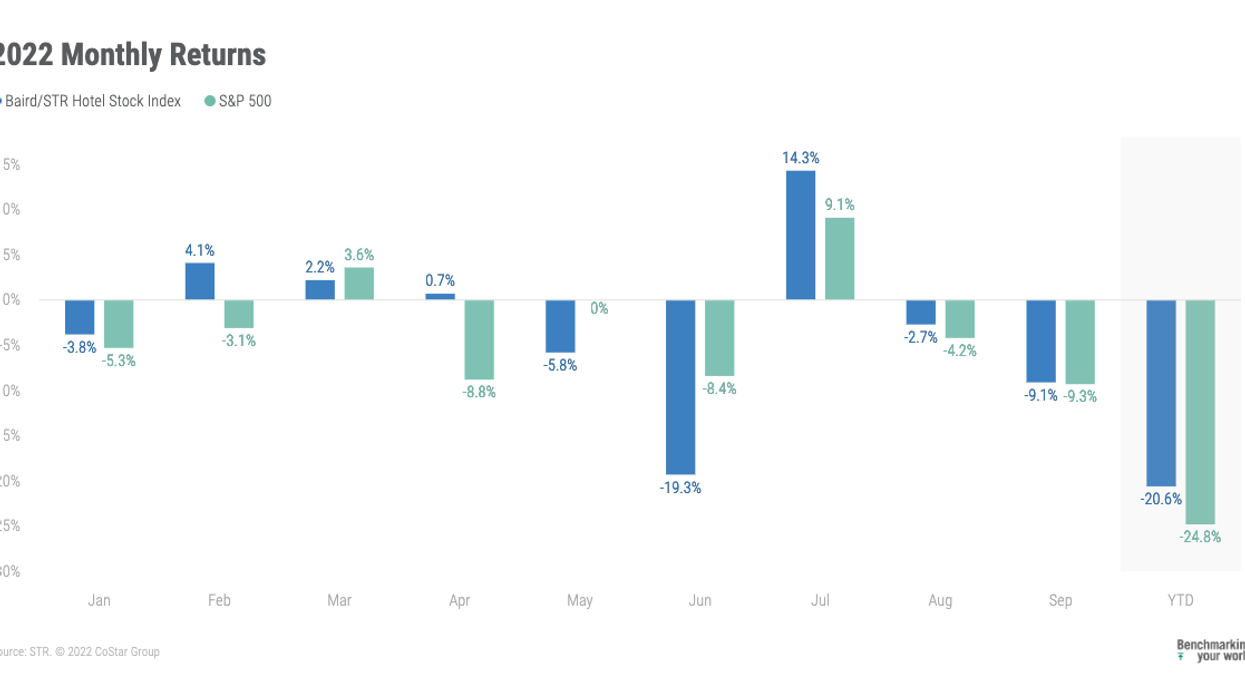

THE BAIRD/STR Hotel Stock Index fell 9.1 percent in September, according to STR. Experts said that they have concerns regarding recession and its impact on the sector.

The index witnessed a sharp drop of 20.6 percent year-to-date through the first nine months of 2022. In September, the Index surpassed both the S&P 500, down 9.3 percent, and the MSCI US REIT Index, which fell 12.8 percent. The hotel brand sub-index decreased 7.7 percent from August to 8,268, while the Hotel REIT sub-index dropped 13.5 percent to 989.

“September was a risk-off month for the broader market, and hotel stocks were down sharply as well. However, the Hotel REITs were modest underperformers only, while the Global Hotel Brands were slight relative outperformers,” said Michael Bellisario, senior hotel research analyst and director at Baird. “Broader macroeconomic concerns continue to dominate investor sentiment and positioning, but underlying hotel fundamentals held steady throughout the month, which relatively helped the hotel stocks during a volatile time for the capital markets. Investors continue to ask about recession scenarios and downside analyses for our coverage list, which suggests a lot of the bad news is being priced into the stocks, particularly the Hotel REITs, in our opinion.”

“While a recession is now likely on the horizon, current industry conditions have not yet been affected by a downturn in consumer or corporate spending,” said Amanda Hite, president, STR. “Group demand continues to show strong recovery in our first 'normal' meeting season since 2019. When looking at the leisure segment, weekend room rate growth shows little to no sign of easing, which continues to speak to consumer resilience. Lastly, the decline we've seen in construction activity means new supply will not represent a strong headwind and should only impact select markets such as New York and Nashville.