THINGS ARE IMPROVING for the U.S. hotel industry so far in 2021, and they’ll get even better by the second half of the year, according to CBRE Hotels Research. The ongoing rollout of vaccines against COVID-19 and the passage of the latest federal stimulus package give the research firm cause for a brighter forecast.

CBRE now expects the average national occupancy level to reach 43 percent during the first half of the year and rise to 55.1 percent in the second half, according to the firm’s February 2021 edition of Hotel Horizons. The national vaccination program, which has exceeded 2 million inoculations a day, and the passage of the $1.9 trillion American Rescue Plan Act, said Rachael Rothman, CBRE’s head of Hotels Research & Data Analytics.

“Based on our forecasts, the worst of the top-line declines are now behind us. We are beginning to see green shoots of a recovery in air travel data, booking patterns, and RevPAR,” Rothman said.

Performance will vary, CBRE said, depending on location, property type and chain scale.

“Upper-priced properties will see faster growth in 2021 fueled, by easier comparisons and an uptick in business and leisure travel. However, occupancy levels still will trail those of the mid- and lower-tier properties,” Rothman said.

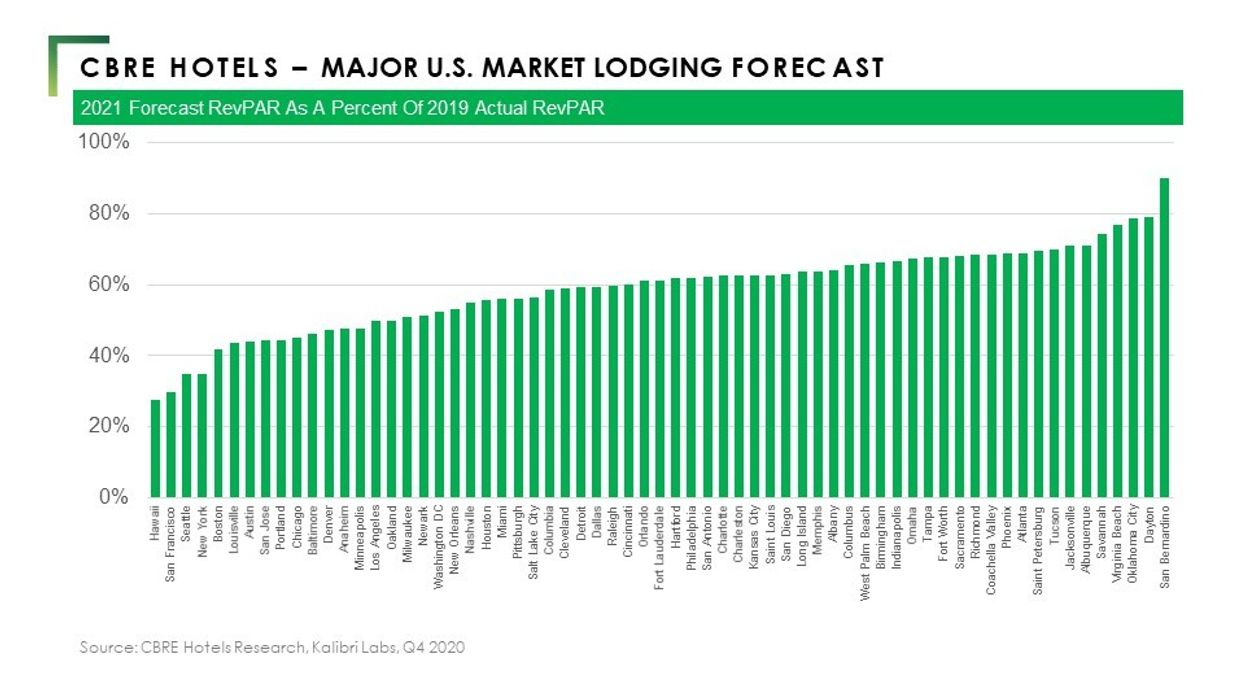

Markets such as Minneapolis, Boston, Chicago and Philadelphia are expected to see RevPAR gains of more than 50 percent during the year but still will fall short of prior peaks. By year end, smaller cities like San Bernardino, Dayton, Oklahoma City, Virginia Beach and Savannah will be closer to returning to 2019 RevPAR levels than other markets.

Beyond 2021, CBRE forecasts a return to 2019 RevPAR levels in 2024. In general, lower-priced properties will recover sooner than the higher-priced hotels.

“One factor supporting enhanced lodging performance in the second half of this year and beyond is a reduction in the traditional lodging supply,” CBRE said in its press release. “The combination of permanent closures and fewer projects starting construction has resulted in a reduction of CBRE’s hotel supply forecast for 2021 to a gain of just 0.9 percent for the year. CBRE estimates supply growth will remain below 1 percent through 2023. This is less than the long-run average change in supply of 1.4 percent.”

CBRE’s most recent occupancy forecast actually is a little lower for the year than the forecast made in December. At that time, national occupancy averages were expected to be 44.4 percent for the first half of the year and 55.7 for the latter half.