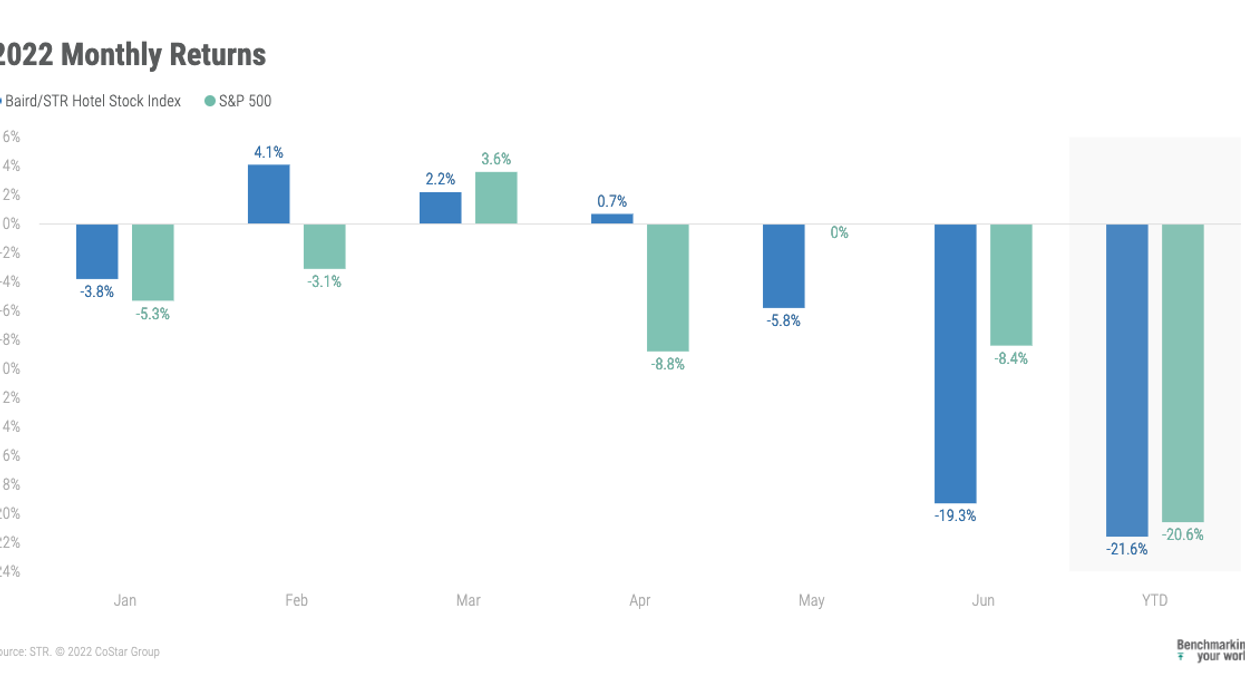

THE BAIRD/STR HOTEL Stock Index dropped in June for the second consecutive month. The index dropped for the first time, after rising continuously for five months, in May.

Baird/STR recorded a sharp fall of 19.3 percent in June, according to STR. The index dropped 5.8 percent in May. It went up 0.7 percent during April. It increased 2.2 percent in March after rising 4.1 percent in February. The index decreased 21.6 percent during the first six months of 2022.

The Baird/STR Index fell behind both the S&P 500, dropped 8.4 percent from May and the MSCI US REIT Index, down 7.9 percent respectively during June. The hotel brand sub-index fell 19.3 percent from May, while the Hotel REIT sub-index dipped 19.5 percent during the month.

“Hotel stocks continued on their downward trajectory in June and were significant relative under-performers as investors began to factor in an increasing likelihood of an impending recession,” said Michael Bellisario, senior hotel research analyst and director at Baird. “While the upcoming summer travel months are expected to be strong, investors are looking beyond the near-term fundamental strength to a period when demand and ADR growth are likely to moderate, which is supported by the many macroeconomic indicators that are flashing signs of broader slowing.”

“With summer vacation season in full swing, pandemic-era highs in room demand have demonstrated the sustained desire from Americans to travel,” said Amanda Hite, STR president. “While beach destinations continue to thrive, we have seen downtown locations, which were lacking both corporate group and transient demand, post encouraging results. Room rate growth continues unabated across all chain scales, and it is good to see upper upscale hotels being able to capitalize on renewed interest. At the same time, the macroeconomic sentiment has shifted with a 'hard landing’ expected for the U.S. economy in 2023. Developers and owners are watching the interest rate environment closely, and recent rate hikes will likely have a measurable impact on the construction pipeline going forward.”